The performance of cooperative insurance received the seal of approval of the shareholders

According to the financial news report, citing the public relations of Cooperative Insurance, the annual general meeting of Cooperative Insurance was held at the Simorgh Hotel with the presence of 79.59 percent of shareholders and the presence of officials such as Ali Ostadhashmi, the deputy supervisor of Central Insurance and Seyed Mohammad Karimi, the secretary general of the insurance syndicate. It was held in Iran.

In this event, the Secretary General of the Syndicate of Iranian Insurers stated: It is the shareholders with whom the business market prospers, turns the economic wheel of the country and creates hope in the youth.

Karimi, pointing out that Mr. Mazloumi is one of the competent managers and has passed the industry exam, stated: I have a special relationship with the cooperative insurance, the cooperative and the rules of the cooperative could not be reconciled with the rules of the stock exchange, and a lot of effort was made for that. Although we must note that the cooperative culture is basically rooted in insurance.

He went on to say: I sincerely thank the shareholders, especially the real shareholders, because buying insurance shares is a social responsibility and the person has actually worked hard to repair damages in a charity organization.

The Secretary General of the Syndicate of Iranian Insurers further pointed to the operational status of the Cooperative Insurance Company and explained: The low loss ratio is not important, but the low loss ratio is important, and the loss ratio of 71 for the Cooperative Insurance Company is commendable. When the loss ratio is low, it means that there is a profit due to the insurance, and this means that the CEO and the board of directors have put in all their efforts.

In the following, Younes Mazloumi, CEO of Cooperative Insurance, pointed to the presentation of the company’s performance report last year and stated:

Among the most important achievements of the company in 1401, the following can be mentioned:

1) Realization of profit of 400,943 million Rials

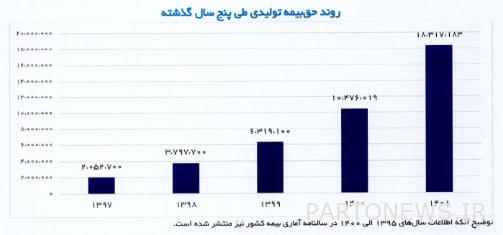

2) Production insurance premium amounting to 18,317,183 million rials, which shows a 75% growth compared to the previous year.

3) Implementation of capital increase from the amount of 1500 billion Rials to 5000 billion Rials

4) The lowness of the loss factor of the company compared to the average of the insurance industry, which is 7,508,115 million Rials in this period and the total loss ratio of the company is 41%, which is lower compared to the 57% loss ratio of the insurance industry.

5) Maintaining the rank of financial wealth level one

6) Obtaining short-term A1+ and long-term -BBB credit rating in re-evaluations as the first insurance company

7) renewal of ISO 9001 quality management standard certificates; ISO 10002 customer complaint handling standard; ISO 10004 customer satisfaction standard and ISO 31000 risk management standard.

He also referred to “sales performance” in the next section and said:

Cooperative Insurance was able to achieve more than 18 billion Rials in insurance premium production in 1401 by realizing more than 96% of the approved budget and growing by 75% compared to the same period of the previous period.

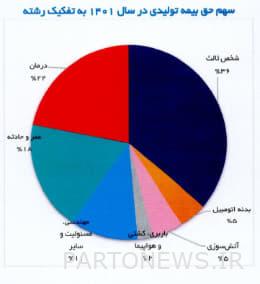

In the same period, the composition of sales of different insurance fields was as follows:

It is noteworthy that the company, while controlling the amount of medical insurance sales, which in recent years is considered one of the fields with a high loss ratio due to competitive rates as well as the increase in medical costs, by increasing the share of other insurance fields in the insurance portfolio. While being aware of the added value of health insurance services for customers, reduce the share of health insurance from 35% in 1400 to 22% in 1401.

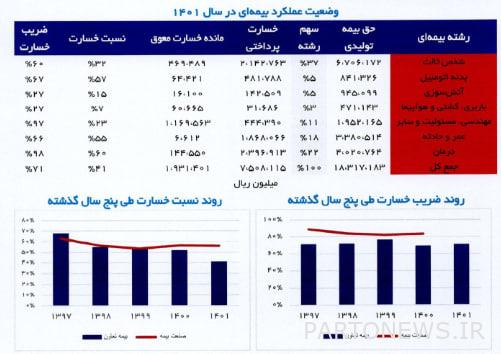

Mazloumi also explained in the “performance of insurance claims” section:

In 1401, Cooperative Insurance was able to achieve a loss ratio of 41% and a loss factor of 71% by controlling insurance risks through portfolio portfolio management and selecting insurable risks. They are in a favorable position.

The amount of medical insurance claims in 1401, although in Riyal terms, has grown by 17%, but with proper control and selection of insurance risks, the medical insurance claims ratio has decreased by 9% and reached 95%. Meanwhile, the insurance industry has been faced with the increase in treatment tariffs and the removal of preferred currency.

In terms of car insurance, in terms of contractionary policies based on accepting appropriate risks and not entering high-risk markets, this sector includes motorcycle insurance, autobar-autocar, intra-urban transport fleet and similar cases, as well as focusing on the zero vehicle portfolio. Km has controlled the amount of damage.

The CEO of Cooperative Insurance also mentioned in the explanation of “market share”:

Aiming to achieve a market share of more than one percent in 1401, Cooperative Insurance has been able to achieve this goal with a stable growth.

He also explained in the explanation of “operational and financial ratios”:

Based on the reported performance, the status of some operational and financial ratios in cooperative insurance is as follows:

The CEO of Cooperative Insurance finally pointed out the “important measures implemented in 1401” and explained separately:

A) Risk Committee:

Updating and identifying more than 270 risk cases in the fields of fire insurance, liability insurance, engineering insurance, personal insurance, cargo insurance, car insurance, reinsurance, research and development, training, branches, resources human, public relations, communication with customers, representative affairs, legal, risk management, financial affairs, information technology, tender affairs, physical building risks; focusing on the analysis of some case insurance risks; Conducting risk management training courses at the company level; Analyzing the relationship between strategic risks and identifying key strategic risks and planning to conduct stress tests based on the identified cases; Approval of risk appetite document.

b) Insurance technical units (medical, automobile, engineering and liability, life, fire, cargo, ship and plane insurances):

B-1) New products and services:

Domestic travel accident insurance policy (for incoming passengers)

Revising the table of age and capital of life insurance and increasing death capital up to 2 billion tomans

Ship owners insurance, p&i covers and other marine insurances

Liability insurance of aircraft owners and airport services

Transit freight insurance

Sharing experiences of cooperative insurance in the field of innovation in the Tavino framework at the industry level

B-2) Improving the quality of services:

Providing 24-hour support services in cargo, ship and plane insurances according to the time difference in different countries

Holding numerous meetings with insurers of different disciplines to resolve ambiguities

B-3) control of damage coefficient:

Investigating major insurance risks and tenders in technical committees

Dealing with all third party insurance damage cases, especially injury cases before the end of the year and preventing the day of payment.

Applying restrictions on the issuance of body and third party insurance for some damage-causing vehicles

c) Reinsurance:

Monitoring of insurance policies with high storage capacity and checking the paid losses of insurance policies with optional assignment on a continuous basis

Reducing discretionary transfer by reviewing the performance of participation contracts and capital surplus and improving the status of contracts according to the need at the time of renewal

Failure to assign favorable risks in proportion to storage capacity

Preparation of statistics on accumulation of earthquake and flood risk on a provincial basis and control of risk accumulation in each province

Conclusion of an open cover contract to cover the liability of ship insurance policies

Preparation, adjustment and follow-up of settlement of all types of reinsurance invoices

d) Information technology:

Redesigning and unveiling the new website of Dr. Bimah

Creating the infrastructure of the system of gratitude for medical insurance

Launching the online application of body insurance (Apollo)

Preparation of infrastructure for the new product of mileage insurance

e) Affairs units of branches and provinces; and affairs of agents and brokers

Establishment of 6 new branches in Ilam, Birjand, Khorramabad, Shahrekord, Qom and Yasouj

Periodic performance evaluation (weekly, monthly and yearly) of branches and performance improvement planning

f) Public relations and customer affairs:

Extension of ISO 10002 and ISO 10004 certificates in dealing with complaints and customer satisfaction

Received consumer rights protection certificate for the third year in a row

Using software to communicate with customers

Forming a VIP customer committee and extracting a customer rating model

Obtaining the title of top customer satisfaction rating in the insurance industry public relations festival

Implementation of the second course of insurance industry speech competition (Insurtalk)

Obtaining the title of the second place of social studies and researches in the public relations festival of the insurance industry

Designing and publishing the cooperative insurance brand book

Decisions made

Finally, after listening to the reports presented by the CEO, reports from Mohsen Tanani, the representative of the auditor organization; Samira Karji, the representative of the Securities and Exchange Organization and Amir Mirzaei, the representative of the Central Insurance Company, spoke.

In the following, due to the end of the activity period of the auditor organization, a vote was held by the shareholders to elect a new auditor organization and under the supervision of “Alireza Saqaei” and “Ahmed Ahmadi” as the first and second supervisors elected by the shareholders, “Audit and Services Institute” Arya Nagar Data Management” was chosen as the main auditor and “Experienced Audit Institute” as the alternate auditor.

On the other hand, with the approval of the shareholders, a dividend of 70 Rials per share was distributed and “Information Newspaper” was also selected as the official newspaper of the company.