What is the dangerous signal for the stock exchange / interbank interest rate?

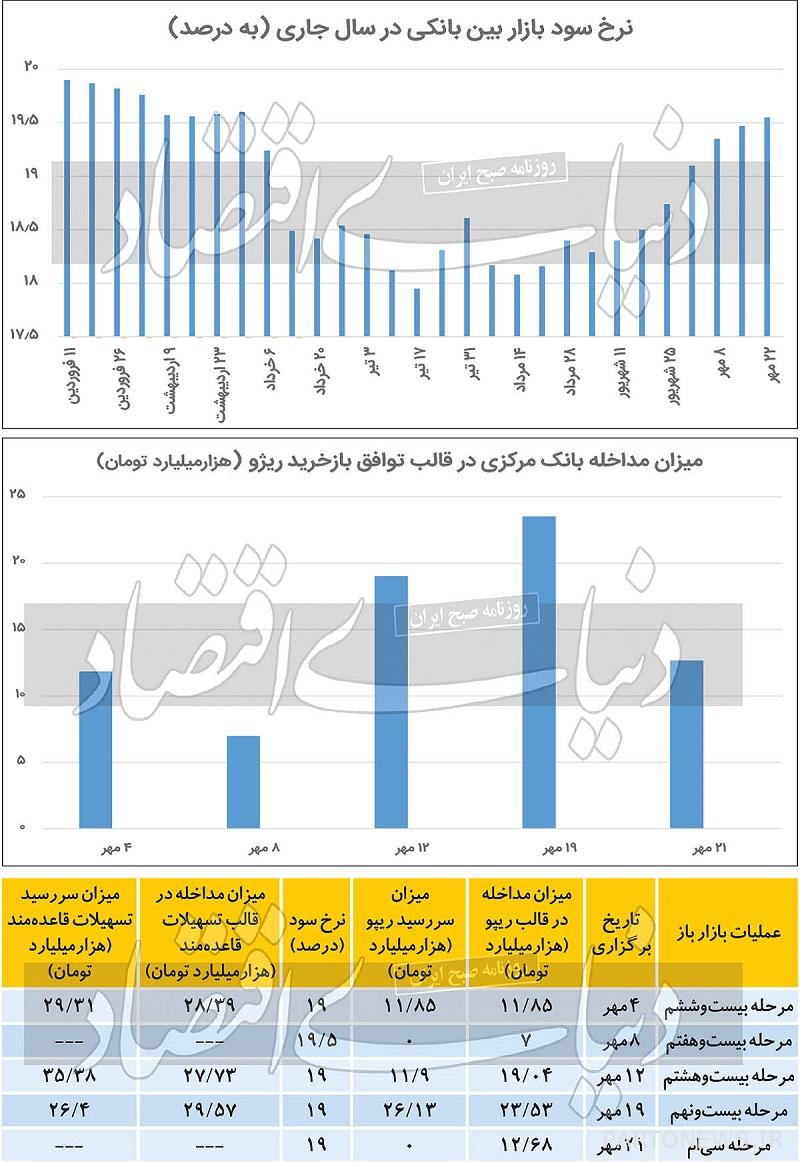

According to Tejarat News, the official statistics of the Central Bank show that the interest rate of the interbank market has increased by about one percent from 18.5 percent to 19.6 percent in the last month.

A review of statistics indicates an increase in the thirst for demand for resources; As in the last 5 stages of open market operations, a total of 74.1 billion tomans has been injected into this market. Due to the reduction of government borrowing from central bank resources, which was mainly located in banks, the money supply in banks’ transactions has decreased and the interbank market interest rate has increased.

A review of official reports shows that for the first time, two phases of open market operations took place in less than a week. These steps form the twenty-third and thirtieth stages of the implementation of these operations by the monetary policymaker.

During these stages, the Central Bank agreed to implement open market operations in the form of repo repurchase agreements at the rate of 23.53 and 12.68 billion tomans, respectively, with a weekly maturity of at least 19%.

In other words, the injection of resources in the amount of 36.21 billion tomans and the increase in the amount of intervention in the form of regular facilities by the policymaker contains several important points: The first is that this case shows the thirst for demand in the interbank market.

The second case is that there has been a decrease in resources in the interbank market.

The third case is the implementation of the above operations by the policymaker to control interest rates in the corridor and return the interbank market rate to its equilibrium. According to official statistics, the interbank market interest rate, which reached 18.29% on September 25, had an upward trend in the last eight weeks; As it reached 19.55 percent on 22 October. This shows that although policymakers have put resource injection operations on the agenda in the last five weeks, interbank market interest rates remain bullish.

Fourth, the 13th government is facing a high budget deficit and the borrowing ceiling from the central bank has been filled in the first five months of the year. Therefore, the government has no choice but to use the bond auction option to cover its non-inflationary budget deficit. Therefore, banks need financial resources to buy securities, and monetary policymakers intervene when resources are scarce. Fifth, the decline in resources in the interbank market indicates a lack of borrowing from central bank resources.

In addition to open market operations, in the 28th week, 7 banks and credit institutions used regular credit worth a total of 29.57 trillion tomans, and in the last stage of this operation, it was not implemented by the monetary policymaker.

Another case is that the analysis of official statistics shows that by the third week of October this year, a total of 99.21 billion tomans of liquidity at a rate below 20% has been injected through open market operations and also 62.79 thousand billion tomans of resources have been absorbed from the interbank market. In total, it can be said that the Central Bank has injected resources equivalent to 36.42 billion Tomans net by the end of the third week of October this year. Finally, after 14 consecutive weeks, for the third time in a row, the total liquidity injection surpassed the total resource absorption.

Details of the last 2 steps of open market operation

The central bank released a report detailing the latest phase of open market operations this year. For the first time in less than a week, two stages of the operation are performed. On October 10 and 11, the twenty-first and thirtieth stages of the open market operation were carried out, respectively.

In order to manage the liquidity required by the Rial interbank market, this monetary institution conducts open market operations on a weekly basis. The operational position of the central bank in these two stages was the injection of liquidity. An examination of the implementation process of the open market operation shows that after 18 weeks when the money-sucking operation was adopted by the policymaker, the liquidity injection operation was used for the fifth time in a row.

According to official reports, in the 22nd phase, 9 banks and non-bank credit institutions participated in the auction. In the mentioned order, the banks and financial institutions sent the purchase order of government Islamic financial securities worth 23.53 trillion Tomans in the form of repurchase agreement (repo) to the Central Bank through the interbank market system. The monetary policymaker took the operational position of injecting liquidity based on his forecast of the liquidity situation in the interbank market.

This position is taken by the monetary policymaker with the aim of controlling and reducing the fluctuations of the interbank market rate around the target rate. Therefore, the Central Bank agreed to implement open market operations in the form of a repurchase agreement in the amount of 23.53 trillion tomans with a daily maturity of at least 19%. In addition, at this stage, the repurchase agreements amounted to 26.13 thousand billion tomans.

In the thirtieth stage, 4 banks and non-bank credit institutions participated in the auction. In the mentioned order, banks and financial institutions sent the purchase order of Islamic government financial securities worth 13.47 trillion Tomans in the form of repurchase agreement (repo) to the Central Bank through the interbank market system. According to its monitoring and forecasting of interbank market resources, the Central Bank agreed to carry out open market operations in the form of a repurchase agreement in the amount of 12.68 trillion Tomans with a daily maturity of at least 19%. In addition, no redemption agreement matured at this stage.

In addition to open market operations, regular accreditation took place during this period. In the week ending October 10, 7 banks and credit institutions used regular credit worth a total of 29.57 trillion tomans. During this period, the amount of 26.4 thousand billion Tomans of the repo performed in the form of regular accreditation matured. But in the last stage of this operation, no intervention was made by the policy maker to carry out regular accreditation operations.

Another case in point is that the central bank’s intervention in the form of regular facilities, which has been reduced since the third week of September; It increased in the twenty-eighth stage. This does not mean that the balance sheet of banks is deteriorating, but it does indicate that the interbank market has been facing a decline in resources over the period. Therefore, it can be said that in the weeks when the level of central bank intervention intensified, there were not enough reserves in the interbank market. In other words, the adoption of the repo operation in the last five weeks and the increase in the amount of intervention in the form of regular facilities have shown the thirst for demand for resources.

Overtaking resource injections

A review of official statistics shows that since the beginning of the year, open market operations have been carried out in 30 stages; However, during this period, the central bank has not taken any action in 11 weeks of liquidity injection policy, in 139 weeks of liquidity absorption and in 6 weeks.

This shows that the central bank chooses its policy every week according to the monitoring of resources in the interbank market; In the weeks when banks are facing depletion of resources in the interbank market, the central bank’s policy of injecting liquidity through repo operations, and on the other hand, in the weeks when the market is facing increasing resources, the policy of this monetary institution to manage liquidity, repo operations It is the opposite.

In the last five weeks, the monetary policymaker has recognized the decline in resources in the interbank market and has therefore based his position on repo operations. This intervention has been adopted by the policymaker to control the interest rate in the corridor and return the interbank market rate to its equilibrium.

Another case is that the analysis of official statistics shows that by the third week of October this year, a total of 99.21 billion tomans of liquidity at a rate below 20% has been injected through open market operations and also 62.79 thousand billion tomans of resources have been absorbed from the interbank market.

In total, it can be said that by the end of the third week of October of this year, the Central Bank has injected resources equivalent to 36.42 billion tomans in net. Finally, after 14 consecutive weeks, for the third time in a row, the total liquidity injection surpassed the total resource absorption.

Analysis of policy actions

An examination of official statistics shows that the interest rate on the interbank market decreased by a step from 19.9% on 11 April to 17.95% on 17 July, which was the lowest level since the beginning of the year. But it continued to fluctuate with fluctuations; As it reached 18.29% on September 25. The interest rate continued to be on an upward trend, from 18.29% on the 4th of September to 19.55% on the 22nd of October.

This suggests that although policymakers have put resource injection operations on the agenda over the past five weeks, interbank market interest rates continue to rise. On the one hand, this indicates a decrease in resources in the interbank market, and on the other hand, it indicates a thirst for demand in this market.

Economists believe that in the first half of this year, the budget deficit forced the government to borrow money from the central bank. Due to government borrowing and the location of these resources in the interbank market, access to resources was easier. This caused interest rates in the interbank market to decline.

But in recent weeks the policymaker equation has changed; In this way, with the decrease in borrowing and the increase in the supply of securities, the banks’ access to resources has decreased.

This has led to an increase in interest rates in the interbank market since September 25. Another reason is that because the government has opened a special account on the auction option to cover its budget deficit for non-monetary purposes later this year, it is important for policymakers to have access to resources for policy makers through repo operations in the interbank market. he is doing it.

Source: the world of economy

Read the latest banking news on the Bank and Trade Insurance صفحه News page.