What was the important signal for the stock exchange / interbank interest rate?

According to Tejarat News, the latest report of the Central Bank shows that at this stage, for the first time, two weekly and occasional auctions were held simultaneously. At this stage, similar to the previous 11 stages, the central bank’s position was to inject liquidity into the interbank market. According to official statistics, in the mentioned stage, about 34.44 billion tomans of resources were injected into the interbank market in the form of repo repurchase agreement and the amount of policy-making intervention in the form of regular facilities was about 1.09 billion tomans.

Despite the repetition of the policy-making procedure in the last 2 months (injection of resources in the form of repo operations in the total amount of 260,000 billion tomans); But there is still the question of why there is a thirst for demand and the interest rate of the interbank market is rising?

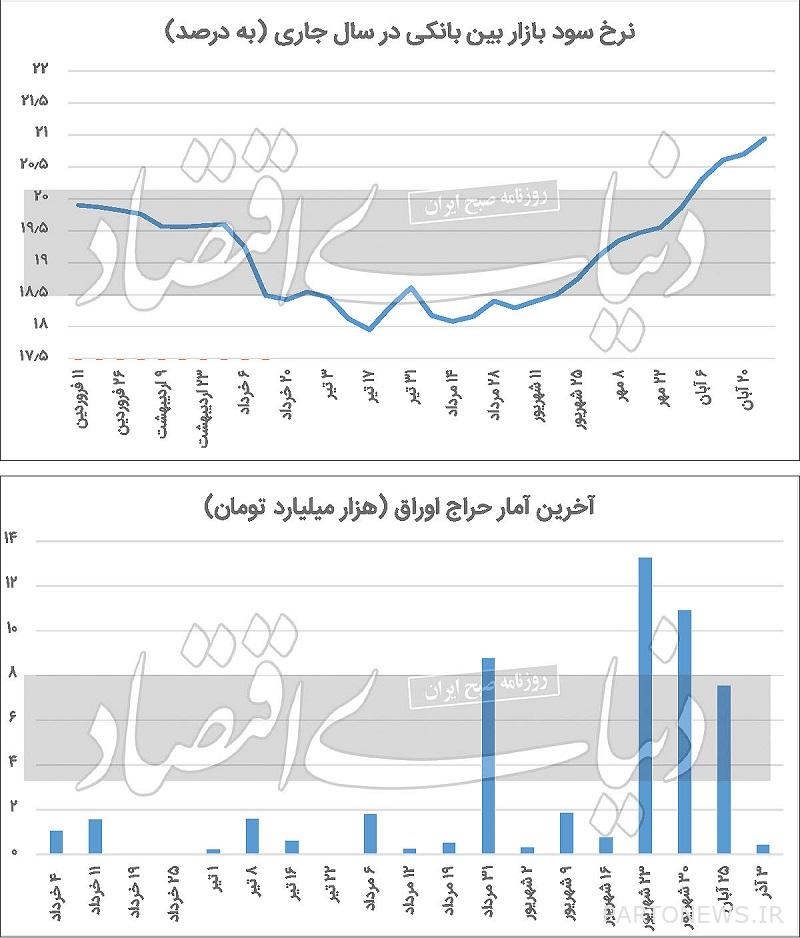

According to official statistics, the interest rate on the interbank market as of September 25, when the interest rate was 18.4%; This index is in a one-way direction so that in the last days of November it reached 20.9%. Economic experts believe that this issue may be due to the formation of an atmosphere of instability and uncertainty in the country’s economy, which is mainly tied to the outcome of Iran’s negotiations on the issue of Borjam; Demand for borrowing from banks as well as inflation expectations is increasing.

In addition, in the last stage of the bond auction operation, 320 billion tomans were financed to banks and non-bank credit institutions and 90 billion tomans in the capital market. in other words; In the mentioned stage, a total of 410 billion Tomans of securities were sold, which has decreased by 720 thousand and 120 billion Tomans compared to the last stage.

It seems that the new government has activated the non-inflationary option of the bond auction to cover its budget deficit, but has not taken the necessary care for this issue, so that after a break of nearly 2 months from closing the bonds while hoping to Last week, the boom will return to securities and this ambiguity mechanism will be removed, but in the last stage of the auction, we are witnessing a recession in this market.

This is despite the fact that the government has already filled the ceiling of the central bank’s salary withdrawals and can no longer finance it from here. The obvious question is that while the only non-inflationary way to finance the budget deficit is to use the option of issuing bonds; What is the government’s plan to cover its deficit by the end of the year?

Details of the last stage of monetary policy

On the first day of December this year, the latest report of the Central Bank on monetary policy operations was published. This is the 36th phase of open market operations this year.

This monetary institution implements the open market policy on a weekly basis in order to manage the liquidity required by the Rial interbank market and also to smooth the resources in the banking network.

According to official reports, the operational position of the central bank at this stage was similar to the previous 10 stages, liquidity injection; In this way, during this stage, a total of 34.44 thousand thousand billion Tomans intervened in the form of repo operations. Another is that in the mentioned stage, the amount of 34.58 trillion tomans of repurchased agreements was matured.

In addition to open market operations, the central bank also conducted regular lending operations during this period.

According to official statistics, the amount of policy-making intervention in the form of regular facilities was 0.09 thousand billion tomans and the equivalent of 15.15 thousand billion tomans was due from the implementation of this policy. Another is that for the third time in a row in the mentioned week, in addition to the weekly auction, a occasional auction is held, with the difference that both of these auctions are held on the same day and without time interval.

Net policymaker intervention; 222,000 billion

In order to have a more comprehensive view of the implementation of monetary policy by the monetary policymaker; It is enough to review the statistics of these operations from the beginning of the year. A review of official statistics shows that since the beginning of the year, open market operations have been carried out in 36 stages; However, during this period, the central bank has not taken any action in 17 weeks of liquidity injection policy, in 139 weeks of liquidity absorption and in 6 weeks.

This shows that the central bank chooses its policy every week according to the monitoring of resources in the interbank market; In the weeks when banks are facing depletion of resources in the interbank market, the central bank’s policy of injecting liquidity through repo operations, and on the other hand, in the weeks when the market is facing increasing resources, the policy of this monetary institution to manage liquidity, repo operations It is the opposite.

Therefore, it can be said that the central bank in the last 11 stages of monetary policy operations, considering the reduction of resources in the interbank market, took the position of injecting resources. Despite the policy of the policy-maker in the mentioned stages, the injection of resources in the form of repo operations in the total amount of 260,000 billion Tomans; But there is still the question of why there is a thirst for demand and the interest rate on the interbank market is rising. in other words; Although the central bank has been conducting repo operations since the beginning of the fall, it has not yet been able to stem the rise in interest rates in the interbank market.

Economic experts believe that this is due to the formation of an atmosphere of instability and uncertainty in the sphere of the country’s economy, which is mainly the result of Iran’s negotiations on the Borjam issue, and the demand for resources in the interbank market and rising inflation expectations. In addition, the analysis of official statistics shows that by the first week of December of this year, a total of 285,000 billion tomans of liquidity at a rate of 20% has been injected through open market operations and also 63,000 billion tomans of resources have been absorbed from the interbank market.

In total, it can be said that the Central Bank has injected resources equivalent to 222,000 billion tomans in net terms up to the mentioned period. Finally, for the ninth time in a row, the total liquidity injection has surpassed the total resource absorption.

Twentieth auction details

In addition to monetary policy, a bond auction policy was held this week. The auction is the twentieth stage of the auction of government Islamic securities this year and the sixty-first stage of the implementation of the policy since the launch of this policy last year.

The Ministry of Economy does this in order to finance non-inflationary government by issuing and issuing government securities among banks, non-bank credit institutions and financial institutions active in the capital market. The mentioned auctions are done through the brokerage of the Central Bank and the quotation system of the Tehran Stock Exchange Technology Management Company.

According to official reports at the mentioned stage, which took place on 3 December; A bank and a non-bank credit institution participated in the auction this week. The bonds offered in this auction were “Arad 92”. The maturity of this bond is in November 1402. The rate of return until maturity of these bonds is equal to 16% and its type is “general marabaha, with coupons and with the payment of interest for 60 months (payment of coupons twice a year)”.

The value of orders sent by banks and non-bank credit institutions through the interbank market system for these bonds was equal to 320 billion tomans, which the Ministry of Economy and Finance agreed with all these orders. In addition, on the mentioned date, 90 billion tomans of bonds were sold in the capital market to other legal entities in the capital market.

Therefore, it can be said that in the last stage of the auction of government Islamic financial securities held this year, a total of 410 billion tomans of government Islamic financial securities were purchased by banks and other natural and legal persons. It has decreased by 120 billion tomans.

Image of securities auction this year

A review of official statistics on securities auctions this year contains several important points; First, before this stage, the government had financed a total of 50,775 billion tomans in the form of bond auctions. Second, three phases of the weekly auctions held this year had not been funded, in other words, the bond auction had taken place. Therefore, it can be said that until the first week of December of this year, the government has sold 51,185 billion tomans of securities.

In other words, during this period, the government has been able to reach 25% of its annual target, which is 200,000 billion tomans. As a result, if the government wants to achieve its set goal by the end of the year and finance itself in a non-inflationary way; In the last 16 weeks of the year, it should sell an average of about 9,300 billion tomans of securities.

The new government appears to have activated the non-inflationary option of auctioning off its securities to cover its budget deficit, but has not taken the necessary steps to do so, after a nearly two-month hiatus from bond closures while hoping to close in the last week. November will return to prosperity and this ambiguity mechanism has been removed, but in the last stage of the auction, we are witnessing a recession in this market.

This is despite the fact that the government has already filled the ceiling of the central bank’s salary withdrawals and can no longer finance it from here. In this regard, the chairman recently mentioned in a meeting with the government’s economic coordination headquarters that efforts should be made to continue the process of financing the budget without borrowing from the central bank until the end of the year.

Finally, out of a total of 5.2 trillion tomans of bonds sold this year, 46.8 trillion tomans occurred during the new government. This means that 91% of the securities sold during the 13th government are a positive point.

But on the other hand, this movement did not continue from 30 September. Economic experts believe that the delay in the implementation of the auction operation caused the government to lose the opportunity for non-inflationary financing during this period; However, in the lost 7 weeks, the government could have achieved a large part of its goal.

Analysis of policy makers’ actions

Previously, several reports have addressed the issue of analyzing policymakers’ actions in financing through the securities auction mechanism. Following the occurrence of a high government budget deficit (about 300,000 billion tomans) and the borrowing of the previous government in the first 5 months of the year to cover the budget deficit, the monetary base experienced a growth of about 13% in the first 4 months of the year.

On the other hand, high borrowing from the central bank’s revolving salary resources caused the withdrawal ceiling to be filled from this place and the 13th government could not finance from this place and turned to other options to cover its budget deficit. Economists believe that the only non-inflationary way to cover the budget deficit is to use the bond auction option.

This option can be the best option in the short term. The government must then think about creating sustainable resources for its revenue generation. Also, because the debt-to-GDP ratio is low in our economy, this option can not cause the government to worry about the increase in debt.

In a report entitled “Bright Engine for Attracting Money”, he explained three scenarios as to why there is high demand in the interbank market despite the high infusion of liquidity and the rising interest rate of the interbank market; The increasing trend of lending facilities of banks in the last two months, turning to indirect borrowing from banks following the filling of the direct borrowing ceiling and finally the transfer of long-term to short-term deposits following the intensification of uncertainty and instability in the country’s economy.

In another report entitled “Return of Bonds; “On the policymaker’s desk” he pointed out that the government, after a two-month hiatus in holding the weekly auction; He took a new initiative and used a new tactic in holding the weekly auction, using for the first time this year a bond payout frequency of less than a year. This shows that the policymaker is changing the tactics to make the securities auction market more attractive. However, economists believe that this method in a situation where inflation is high; It will not have a high impact.

Finally, in a report entitled “Stormy Return of Bond Auctions”, he addressed the issue that in the last stage, the government financed 7,530 billion tomans worth of weekly bond sales, which is equivalent to 920 billion tomans through banks and non-bank credit institutions. 610 billion tomans was done through the capital market.

This shows that, firstly, in an atmosphere of economic uncertainty, the acceptance of individuals and financial and investment institutions (such as fixed income funds) as a cover for inflation risk has increased and on the other hand, the stock market is not a competitor for the securities market.

Source: the world of economy

Read the latest banking news on the Bank and Trade Insurance صفحه News page.